Making a Party out of Project Management: Chapter 4 - Paying for the Party - Part 1 of 2

- Jul 28, 2025

- 6 min read

Updated: Sep 20, 2025

As a thank you to her friends, Abby came up with an idea to “pay” them for their help. She wanted to surprise them after the party with a carnival ride punch card for the fair that would be in town the next weekend. Would this fit within the cost constraint set by her parents? There were a few different prices to choose from, and she thought it would be great since the fair was such a special event for them every year. To get it all worked out, Abby made a plan to determine how much the project would cost with everything purchased and then added to that the cost of getting a punch card for each of her friends.

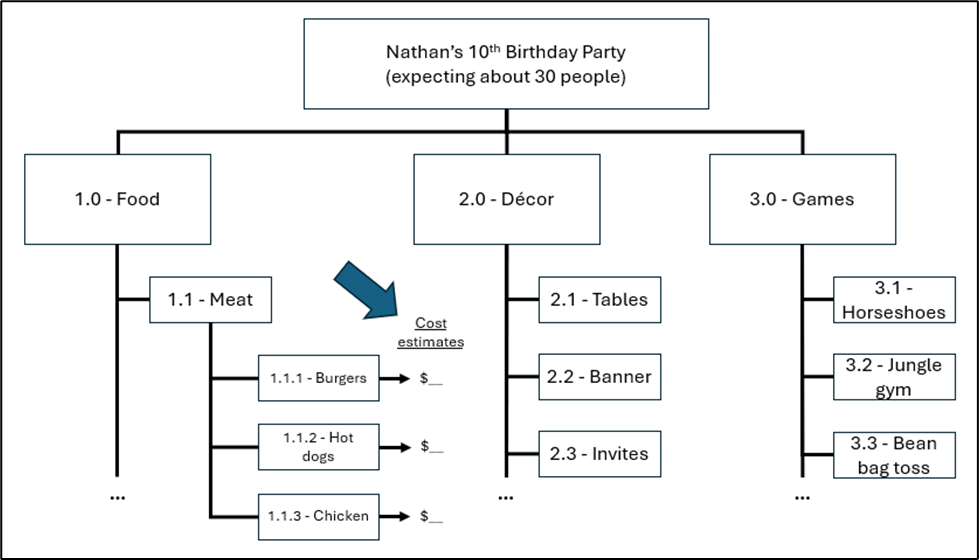

Abby needed to plan cost management to help her to estimate the project’s costs. She reasoned that each piece of scope for the party would have some kind of cost associated, at least for purchased or rented items. Even for something like making the cake at home, there would be a cost of ingredients. If the money isn’t there to buy what’s needed for a piece of the project scope, how will that scope get accomplished? So, Abby created a copy of her WBS that she could use to record cost estimates for each WBS item. For now, she was just making the template but would use it soon when it came time to estimate costs.

Copy of WBS for adding cost estimates for items.

Once Abby had estimates of the project’s costs, she would need to make sure those paying for the project agreed that the costs were reasonable. In other words, as the project manager, she would present her cost elements and overall cost estimate to the project sponsors for their approval. If they thought the project was too expensive, she would have to discuss with them how to reduce the cost, probably by choosing some scope items to reduce or eliminate and thereby cutting their corresponding costs. In addition to initial approval of the budget, Abby also wrote down what she would do to ensure Mom and Dad approved any changes in spending in case something ended up being more expensive than planned. She figured running requests for additional spending by them ahead of time was better than overspending and then trying to explain it after the fact.

After getting costs estimated and a budget approved, Abby would need a way to control costs. Again, this meant control in the project management sense, so tracking how money was being spent and making adjustments to spending if the actual spending was significantly different from the planned spending. In project management, the practice of gathering and analyzing data for controlling both cost and schedule is known as earned value management [14]. To get started on this, Abby was able to make a simple spreadsheet table with each day of the project across the top row, and the row below that having the budget to spend for that day, known in project management as planned value [15]. Knowing that the actual work might not go exactly to plan, Abby included a row for earned value [16] to measure how much of the planned value was accomplished by the end of each workday. Lastly, Abby created a line for actual cost [17] in the bottom row, so she could easily compare the anticipated cost of the project and what was achieved against what was actually spent.

[14] Project managers perform earned value management to track cost and schedule health for their projects by taking three basic measurements: planned value, earned value, and actual cost. Various metrics are computed from these three raw data measurements.

[15] Planned value is the scheduling of daily project activities in the form of dollars spent instead of time taken to perform the activities. If $200 worth of activities are planned to be accomplished on a given day, that day’s planned value is $200.

[16] Earned value is the monetary measure of how much work was actually accomplished on a given day. If the planned value for the day was $200, but only $180 worth of activities were completed, the earned value for the day would be $180. Earned value is compared to planned value to assess project schedule performance.

[17] Actual cost is the measure of how much money was spent. If the planned value for the day was $200, and the earned value was $180, but only $160 was spent to accomplish the $180 worth of work, the actual cost for the day is $160. Actual cost is compared to planned value to assess project cost performance.

Budget spreadsheet template.

Later on, after the end of the project, Abby would use her spending information to create an expense report to verify the exact actual cost of the project and reconcile it against the debit card balance that Mom and Dad would loan her to use for the project. Since Abby was tracking planned and actual costs in order to control cost, this would be pretty straightforward and would be bundled with receipts from every transaction into a report for her parents to review. This is one of the last things Abby would complete the day after the party, once all transactions had been finalized.

With the process for estimating the required project costs in place, Abby was ready to go through the items in scope for the project and make a reasonable guess at how much each would probably cost. She based these estimates on the costs of things like cake ingredients from the grocery ad, checking the city website for a park pavilion rental fee and looking at party packages for renting party games and gear.

Cost estimates added for WBS items.

After completing and adding up all the WBS item cost estimates, Abby next made a three-point estimate for the cost of the different punch cards she considered buying for each of her friends:

- A 5-ride pass for $7

- A 10-ride pass for $10

- A 15-ride pass for $14

Abby had seven friends helping with the party, so for the seven punch cards she would need to buy, she had three points of cost that ranged from $49 to $98. While a 5-ride pass was better than nothing, Abby felt they were giving her enough help to deserve more than that. On the other hand, if her friends did a lot more work than expected to put the party together, Abby was going to make the case to her parents that they should get the 15-ride pass. But really, she knew they would likely agree on the 10-ride pass being the most appropriate option, since the $28 dollar cost difference between those two options made a substantial difference in the cost of the party.

After totaling the cost to do all the work, including the cost of the punch cards, Abby finally had activity cost estimates for the project. This was supported by a basis of estimates; cost estimates were based on the scope of the WBS and various sources telling Abby the cost of the items needed. She completed relevant project document updates like noting risks of cost variations and how she would keep her parents posted about the budget consumed versus what she was expecting to spend on a given day.

Abby had to make many decisions in the process of estimating the costs. For example, several make or buy decisions were made to balance between the party getting too expensive on the one hand or getting too hard to do on the other. They could have chosen to buy a pre-made birthday cake and saved Mom a lot of baking time, but it would have cost three times what making the cake would. Plus, since Mom loved to bake, it was a no-brainer to make instead of buying this item. On the other hand, the “buy” decision to rent the bouncy castle was easy because it would have taken them days to make one themselves. The “buy” was in quotation marks because they rented instead of buying, with Abby’s parents reasoning that it was only a good deal to buy a bouncy castle if they had plans to use it at least three times, which they didn’t. This was a buy or lease decision where renting made more sense than owning.

Once Abby had estimated the cost of each work package in her WBS, she added them all together with the cost of the punch cards and an allocation for a party package to form a bottom-up estimate, showing how all the individual cost components accumulated into a total project cost.

Next post in the series: Making a Party out of Project Management: Chapter 4 - Paying for the Party - Part 2 of 2